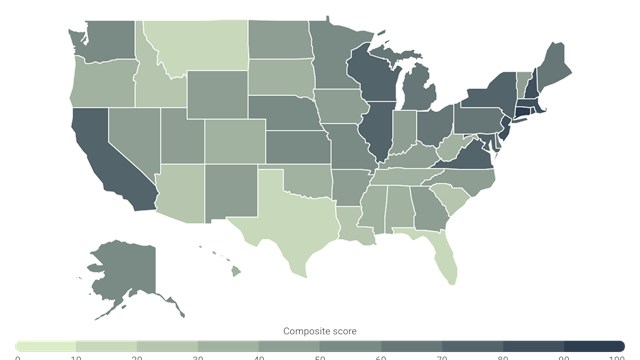

A new study on behalf of construction industry research and analysis firm Construction Coverage using data from Zillow, the U.S. Census Bureau, and Freddie Mac has identified the relative cost of buying vs. renting in nearly 850 U.S. cities and all 50 states.

Price increases throughout the U.S. economy over the past few years have made nearly everything more expensive, but perhaps no spending category has squeezed Americans’ budgets like the cost of housing. Between high costs to buy a home and skyrocketing rents, non-homeowners are faced with impossible choices throughout the market.

Throughout 2020 and 2021, low interest rates and rising household savings and incomes positioned many Americans to buy real estate. But high competition and low supply created a boom in the residential real estate market that sent home prices in the U.S. to record highs. With home prices persistently high and interest rates remaining elevated to tamp down inflation, more would-be buyers have been priced out, increasing the competitiveness of the rental market and in turn driving rents upward. These shifting conditions have made things difficult for households debating whether to buy or rent. Shelter is already the largest spending category for most U.S. households, but larger economic trends have raised the financial stakes on the buy-or-rent decision.

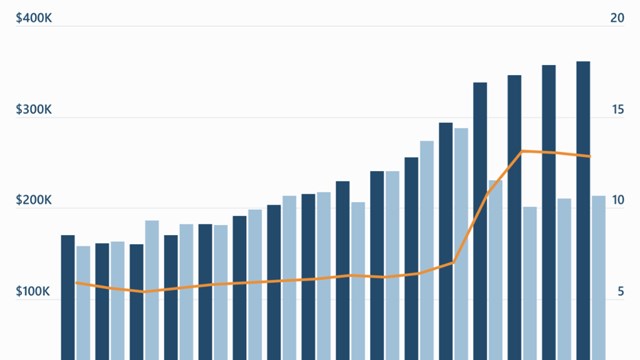

For years, the typical monthly cost of homeownership—after accounting for sale prices, mortgage rates, and property taxes—remained well below the cost of renting in the U.S. The aftermath of the Great Recession, combined with an extended period of low interest rates, kept mortgage payments affordable throughout much of the 2010s. Even as home prices surged in the competitive housing market of 2020 and 2021, historically low borrowing costs continued to make buying a home more financially attractive than renting.

The Shift

However, by 2022, the equation shifted. A combination of soaring home prices and rapidly rising interest rates made renting the more affordable option in most markets. Mortgage rates have more than doubled since reaching record lows in January 2021, and while home price growth has slowed, the median home price remains approximately 33% higher over the same period. As of February 2026, the typical monthly mortgage payment (including property taxes) for a home in the U.S. is now 20% higher than the typical monthly rent.

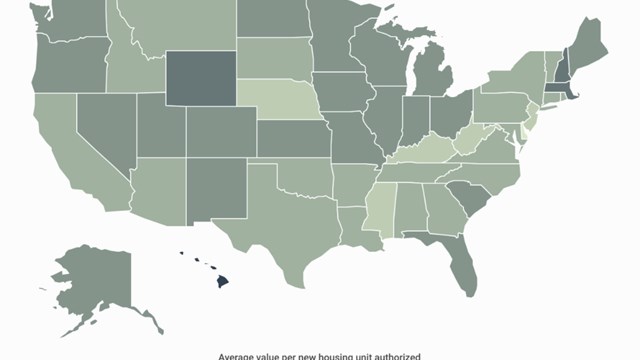

And within some geographic markets, buying is unquestionably more difficult. Locations that face low supply, competitive markets, and high home prices—like cities throughout California and in the greater Seattle region—can be four or even close to five times more expensive for buyers. Cities like fast-growing Draper, Utah, and historic Newton, Massachusetts are also proving especially challenging for buyers.

Out of the 838 U.S. cities considered in this analysis, only 95 are currently more affordable for buyers than renters. Most of these locations are found in Southern states like Alabama, Georgia, and Texas or in Rust Belt locations like Ohio and Michigan. In these locations, home costs remain relatively low, allowing buyers to save relative to the cost of renting.

Here is a summary of the data for New York City:

- Premium/discount of buying vs. renting: +33.7%

- Median monthly mortgage payment: $4,956

- Median rent: $3,706

- Median home price: $812,534

For reference, here are the statistics for the entire United States:

- Premium/discount of buying vs. renting: +20.0%

- Median monthly mortgage payment: $2,274

- Median rent: $1,895

- Median home price: $360,591

{kind=link}

Leave a Comment