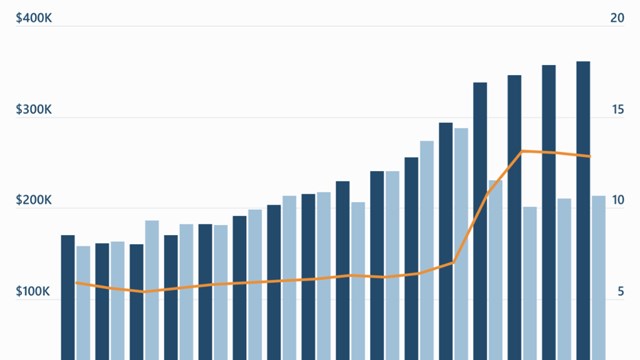

According to a recent press release from the National Housing Conference (NHC), the income needed to buy a median-priced home in the United States has doubled since 2019 from $54,200 to $111,000 - and for new homes, the income required has nearly tripled, skyrocketing from $61,200 to $173,000.

“While the Federal Reserve’s interest rate hikes are beginning to reduce prices, the actual cost of housing remains at historic highs due to the impact of skyrocketing mortgage interest rates,” said NHC President and CEO David M. Dworkin. “As interest rates continue to rise, fewer homes are being built and fewer homeowners are putting their homes on the market for sale. The law of supply and demand cannot be repealed. As long as our supply cannot meet demand, housing will remain unaffordable, and inflation will resist efforts to yield to rising interest rates.”

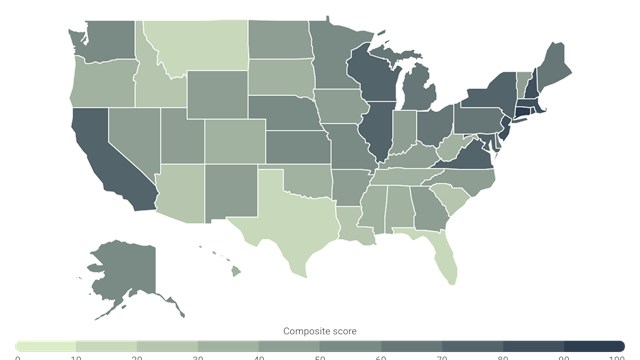

While the staggering cost of renting - much less buying - a home in a major city like New York and its greater metro area has been an issue for decades, Dworkin notes that “The home affordability crisis is no longer an issue reserved for coastal cities. It is impacting homebuyers throughout the U.S.,”

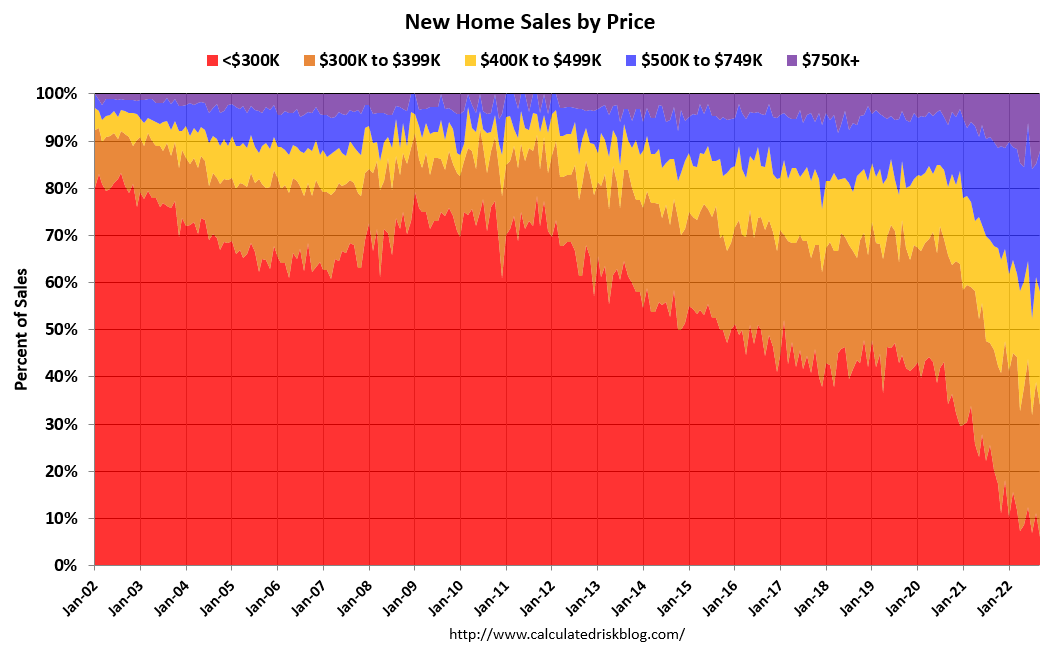

For example, according to the most recent update of NHC’s Paycheck to Paycheck database - which is updated quarterly and enables users to evaluate the affordability of a range of rental and homeownership opportunities for 147 occupations in 390 markets - a pharmacy technician cannot afford to buy a home or rent a two-bedroom apartment in St Louis, Tucson, or Fayetteville, North Carolina. The average police officer in Fayetteville makes $47,310; the average salary needed to buy a home is $65,310. The release also notes that according to Bill McBride’s Calculated Risk Blog, as of September of this year, fewer than six percent of new homes sold in the U.S. were priced under $300,000, down from around 80 percent in 2002.

What’s to Be Done?

According to Dworkin, the solution for reversing this problematic trend is the construction of more affordable housing for both rent and ownership - and it needs to happen quickly. “Congress must pass incentives to build more affordable housing before the end of the year,” said Dworkin, noting that this includes bipartisan legislation like the Neighborhood Homes Investment Act and the Affordable Housing Credit Improvement Act, which together would create 2.5 million homes over ten years. Both of these bills are supported by the National Housing Conference, the Bipartisan Policy Center, and a host of other housing organizations across the ideological spectrum.

NHC’s estimates were based on data from the National Association of REALTORS® Existing Home Sales data, New Home Sales data from St. Louis Federal Reserve Bank using data from the U.S. Department of Housing and Urban Development and the U.S. Census Bureau, interest rate data from Freddie Mac, and mortgage cost calculations by Essent IQ assuming $1200 in annual property taxes and a $25,000 down payment. Income requirements were based on a 30% debt-to-income (DTI) ratio.

Established in 1931, NHC is a nonpartisan 501(c)3 nonprofit organization advocating for affordable housing solutions through dialogue, advocacy, research, and education.

{kind=link}

{kind=link}

Leave a Comment